US PMIs Plunge Into 'Contraction' In Early October, New Orders Weakest Since COVID Lockdowns

- Oct 24, 2022

- 2 min read

Following September's surprise rebound, analysts expected US preliminary October PMIs to be mixed this morning (with Manufacturing slowing while Services ticks slightly higher), but they were very wrong.

Both US Manufacturing and Services surveys shoiwed significant decline in early October, both tumbling into contraction.

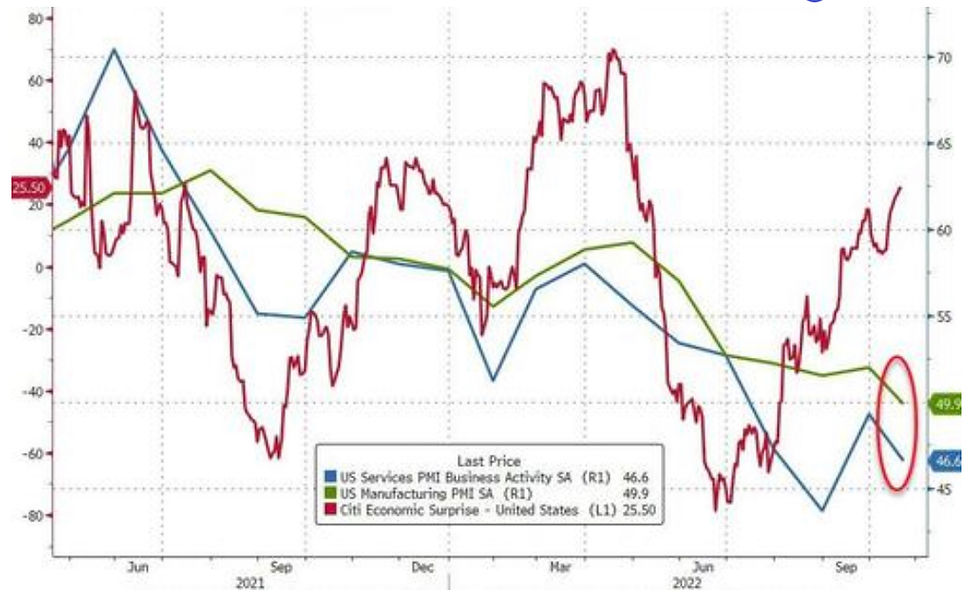

US Manufacturing 49.9 (contraction), below 51.0 exp and down from 52.0 prior

US Services 46.6 (contraction), below 49.5 exp and down from 49.3 prior.

Despite better than expected macro signals...

New orders fell back into contraction territory following a marginal expansion in September. The decrease in client demand was solid and the sharpest since May 2020.

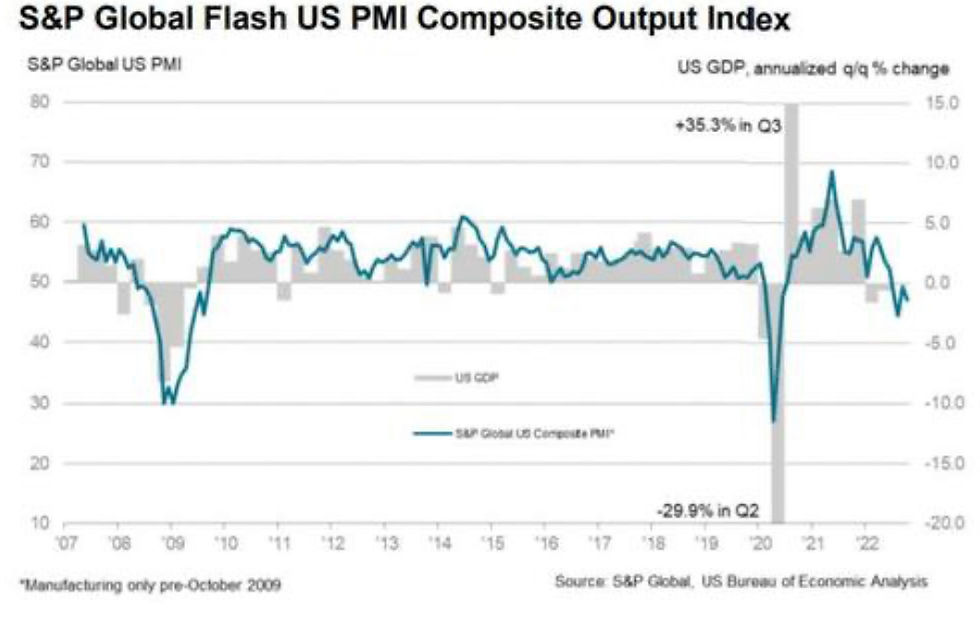

The drop sent the composite index back down to 47.3, in line with the weakness in EU and UK...

Commenting on the flash PMI data, Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“The US economic downturn gathered significant momentum in October, while confidence in the outlook also deteriorated sharply. The decline was led by a downward lurch in services activity, fuelled by the rising cost of living and tightening financial conditions. While output in manufacturing remains more resilient for now, October saw a steep drop in demand for goods, meaning current output is only being maintained by firms eating into backlogs of previously placed orders. Clearly this is unsustainable absent of a revival in demand, and it’s no surprise to see firms cutting back sharply on their input buying to prepare for lower output in coming months. “One upside of this drop in input buying has been a further alleviation of supply constraints, which alongside the stronger dollar have helped cool price pressures in the manufacturing sector.“Although price pressures picked up slightly in the service sector due to high food, energy and staff costs, as well as rising borrowing costs, increased competitive forces meant average prices charged for services grew at only a fractionally faster rate. Combined with the easing of price pressures in the goods-producing sector, this adds to evidence that consumer price inflation should cool in coming months.“The surveys therefore present a picture of the economy at increased risk of contracting in the fourth quarter at the same time that inflationary pressures remain stubbornly high. However, there are clearly signs that weakening demand is helping to moderate the overall rate of inflation, which should continue to fall in the coming months, especially if interest rates continue to rise.”

All of which implies yet another quarter of contraction...

Just don't call it a recession.

SOURCE: ZeroHedge

Comments